While it’s easy to calculate monthly mortgage payments for principal and interest, the total bill — how much cash you actually need at closing — is often fuzzy and mysterious. This happens because all mortgage transactions are unique.

The costs for one $250,000 mortgage can be very different for a second loan of the same size and with the same interest rate.

How much you borrow and the interest rate you pay are no doubt central to loan costs. The catch is that to make sure you’re getting a good deal, you also have to look at other expenses.

While it may seem that some of these additional costs are small, when added together the actual cash involved is no small matter.

There are three pieces of good news here: First, there’s a short, clear, big-type, written summary called a Loan Estimate (LE) that outlines what you can expect to pay at closing. It shows what your financing really costs.

Second, some closing costs can be negotiated and even offset, thus reducing your need for up-front cash. Third, the LE allows you to compare offers from different lenders.

The Loan Estimate (LE) Is A Mortgage Cost Roadmap

Written by the government, the three-page LE form allows mortgage borrowers to easily see costs and compare offers. It’s a roadmap to the costs you will likely face, something lenders must provide within three business days of receiving your application.

Here’s what you might see, using a model form from the Consumer Financial Protection Bureau (CFPB).

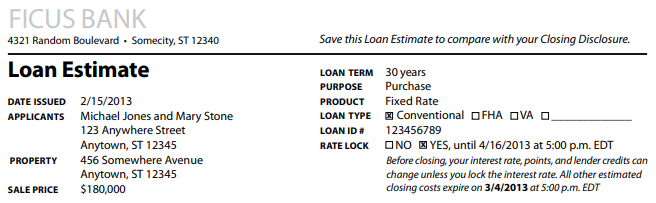

Loan Estimate Form: Page 1

Overview. The LE first shows general loan transaction information such as the property location, sale price, loan amount, and loan term.

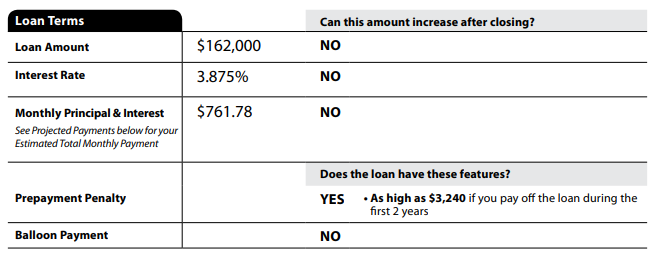

Loan Terms. These are the biggies that get us started: For a fixed-rate loan, you’ll see the mortgage amount, the interest rate, and the monthly cost for principal and interest. There are also forms for other types of loans, such as financing with a balloon note or interest-only payments.

Also, additional information must be provided for adjustable-rate mortgages (ARMs).

Interest rates are always changing, reason enough to shop around for the best rates and terms. Also, if you see a strangely low-interest rate, be sure to check the “Loan Costs” section of the LE.

The lower rate may not be worthwhile if you also see big fees and charges upfront.

You can see that a prepayment penalty is allowed in the sample below, but not all loan programs — including FHA, VA, and USDA financing — do not allow such charges. Balloon payments – loans with a huge final payment – are not allowed with most mortgages.

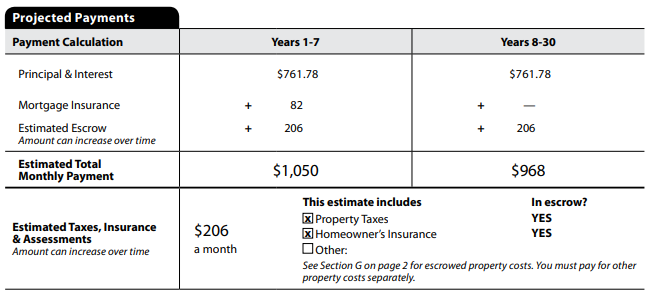

Projected Payments. This section of the LE form looks at the costs you might face during the loan term. CAUTION. While monthly fixed-rate mortgage payments will not change, the story may be very different with mortgage insurance and escrow accounts.

Despite what the form might say, the idea that escrow payments – money set aside by lenders for property taxes, property insurance, etc. – will remain steady year after year is not likely. Taxes and insurance costs routinely increase, just ask any homeowner with a mortgage.

Closing Costs. A summary of projected closing costs is shown at the bottom of the LE’s first page. These numbers are detailed on page two.

Loan Estimate Form: Page 2

While the Loan Estimate’s first page provides a loan overview, page two details costs. This is where to look if you want to follow the money.

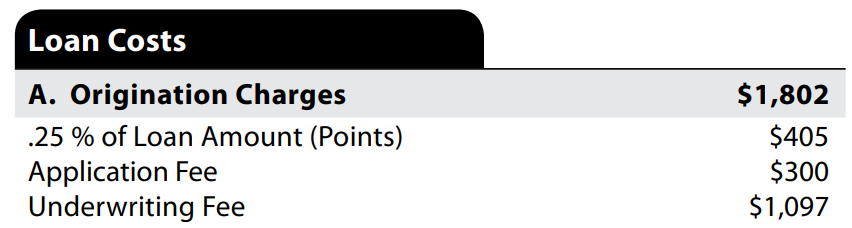

Loan Costs. This block lets you see the real upfront costs for the loan offer. If the loan has a surprisingly low interest rate, it may also have a surprisingly high bunch of fees and costs. This is where you can find them.

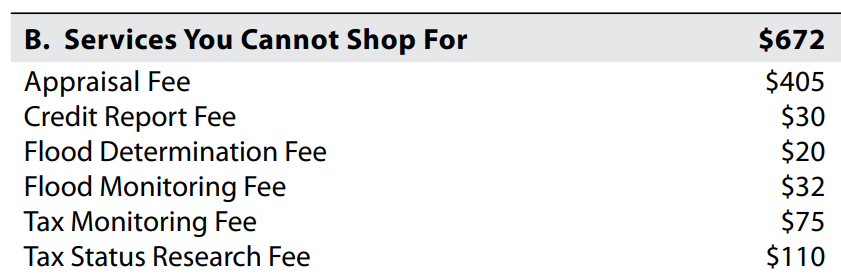

Services you can’t negotiate. These are costs incurred by the lender to originate the loan. In effect, the borrower is paying for services and service providers selected by the lender.

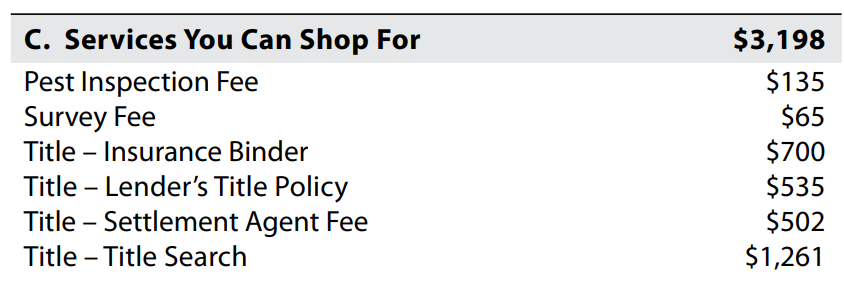

Services you can negotiate. There are some services where you can go into the marketplace and shop for the best deals. If you shop for services, first ask lenders if the company or person you want to use is acceptable to them.

Also, always ask if you can get a title insurance “reissue” rate. This can save a significant amount of money.

The reissue rate may be available if the property was recently financed or re-sold, and you can get a copy of the title insurance policy from the prior sale. For example, if you buy a new home, the land might have been bought recently by the builder.

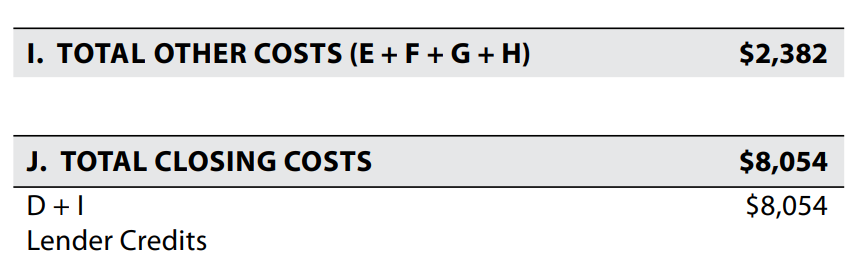

Total Loan Costs. The Loan Estimate form automatically adds up direct loan costs. Closing, however, also includes other expenses, as we shall see.

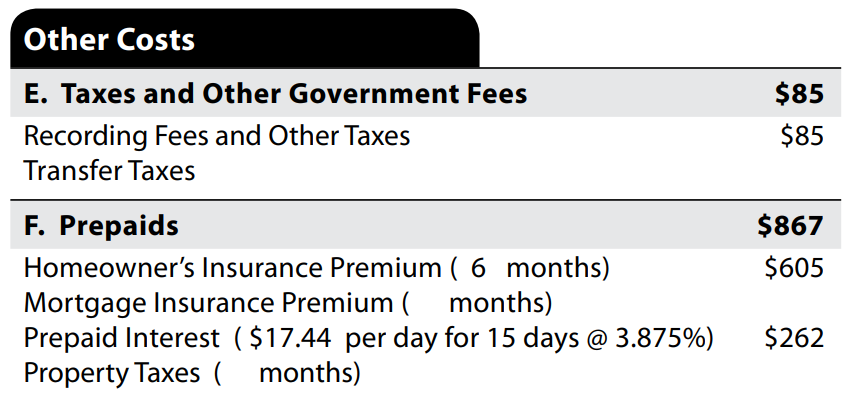

Other Costs. In this section, the LE shows two types of expenses. First, there are government fees. A home sale, financing, or refinancing is a taxable event and a big revenue producer for local and state governments.

Second, the prepaid items are costs for such things as property insurance, mortgage insurance, mortgage interest, and property taxes. In effect, the lender collects some costs at closing before monthly billing begins.

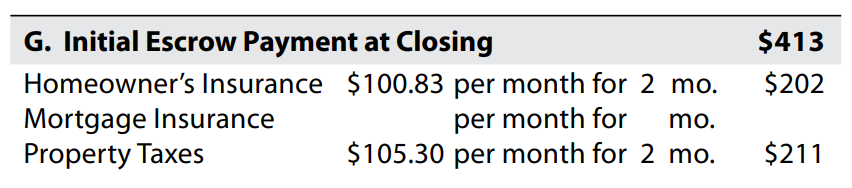

Initial Escrow Payments. Most mortgages require the establishment of an escrow (trust) account, money accumulated by the lender through monthly payments to pay occasional bills such as property insurance premiums or property tax payments. These accounts are started at closing so there’s enough money in hand to meet future costs.

Other costs. This is a section to show items not listed elsewhere. In the case of the model form, there’s a charge for “owner’s” title insurance.

This is different from “lender’s” title insurance in Section C. Lender’s coverage pays off the mortgage balance in case of a faulty title.

Owner’s title insurance covers your purchase equity in the property, though it can cover more with an inflation rider that protects the owner as the property’s value rises. Speak with a title insurance agent for specifics.

Closing costs. Item I shows “other” costs associated with closing, while Item J gives us total closing costs. Notice that with Item J it is possible to include “Lender Credits”. For instance, if you agree to a higher mortgage rate, the lender might pay some closing costs.

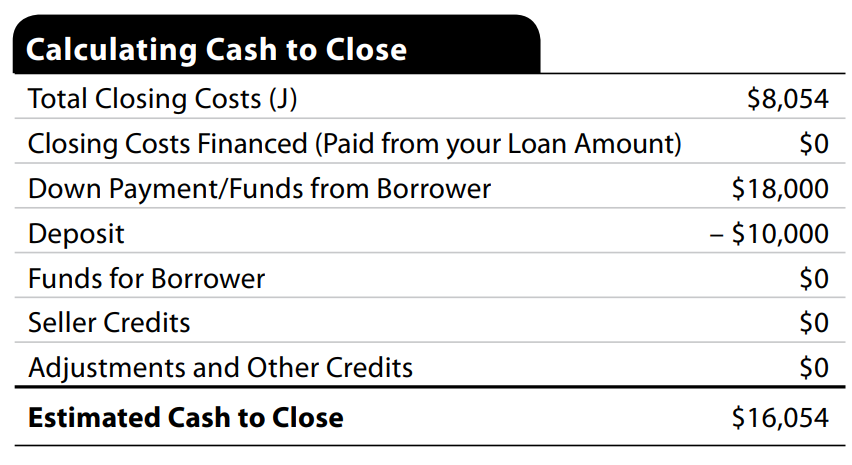

Closing Cash. Here is where borrowers get to the final cost. It shows closing expenses and – for buyers – the required down payment.

It also shows a credit equal to the deposit provided with the purchase offer. Other items that might show up are “funds for the borrower” (perhaps cash from savings), “seller credits” (money from the owner negotiated during the purchase process to offset buyer closing costs. May not be used toward the down payment), and “adjustments and other credit” (miscellaneous items, such as a credit for oil in a tank).

Is the “estimated cash to close” really how much money you need at settlement? It’s likely pretty close, but perhaps not exact because some credits and charges may change. The lender must provide at least three business days before closing a five-page “Closing Disclosure” showing actual closing costs.

Go through this form carefully. Contact the settlement provider immediately if you have any questions. If you expect to make a payment at closing, ask what form of payment is acceptable.

Also, keep additional cash on hand, just in case of a last-minute adjustment. Sometimes such adjustments benefit borrowers. For example, it sometimes happens that mistakes are made and borrowers actually get a credit at closing as a result.

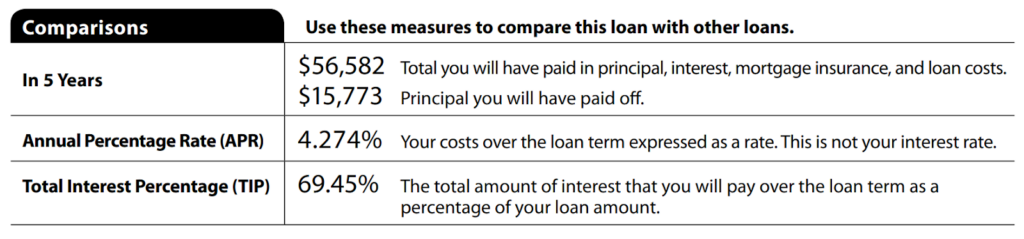

Loan Estimate Form: Page 3

Comparisons. On the third and last page of the Loan Estimate form is are several comparisons figures.

First, you can see the loan’s projected costs over five years, including closing costs. This is a useful way to compare financing options.

Second, you can see the annual percentage rate (APR) and the “total interest percentage” over the loan’s projected term, usually 30 years. Such information is likely not useful because most mortgages last nowhere near 30 years.